Social Housing HMOs

PROPERTY STRATEGY

Explore the possibilities and discover the potential of Social Housing as a Buy to Let Strategy.

Explore Social Housing HMOs for Sale

Looking to purchase HMOs leased to major social housing providers?

These "turn-key" opportunities offer hands-off ownership, contracted rent, and long-term leases—ideal for owners looking for stable, passive income through UK property.

9-10%

7 Year

Contracted Tenancies

NET Yields

New to Social Housing?

Learn the basics of Social Housing as a buy-to-let investment strategy through our introductory video.

Below, we have provided more detailed information about Social Housing as a strategy for Buy-To-Let properties.

A Definition

What is Social Housing?

Social housing is a collective term used to describe housing that is provided by the government, local authorities or housing associations to people or families in need of housing. Social housing aims to ensure that everyone has access to safe, secure and affordable housing, especially those on low incomes or facing other housing difficulties.

Social housing properties are typically rented out to tenants either at concessionary or below-market rental rates. These properties are subject to regulations and eligibility criteria set by the relevant housing authorities. Social housing is essential in addressing housing inequality and providing stable housing options for vulnerable individuals.

Property Types

Social housing can take various forms, and the type of support it provides to its residents often determines the properties used. Single-family houses, apartments, and HMOs are all used by housing associations as social housing, this approach means that properties can be either freehold or leasehold.

Let's tale a look at some of the advantages and disadvantages of social housing.

Social Housing is a great option for those who are interested in the Buy-To-Let market. Housing associations act as tenants for the property owners and offer long-term leases that can last several years. One of the major benefits of social housing is that the rent paid by the housing associations is usually above the local market rate. Additionally, the housing associations typically cover all the expenses that come with owning a property, such as management fees, and repairs and maintenance.

Since the leases are signed for multiple years, you will still receive payment during any vacant periods when the Housing Association is not renting out the property. This makes social housing an attractive option for Buy-To-Let owners who are looking for a stable and reliable source of income without having to worry about the day-to-day responsibilities of managing a property.

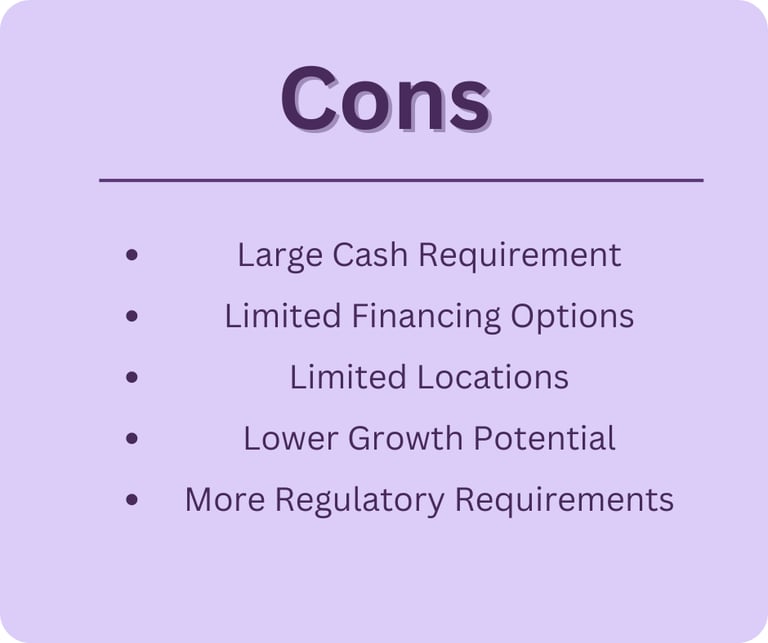

Although there are numerous benefits of owning a property leased to social housing tenants, there are also some downsides to this strategy. One of the primary challenges is the high entry barrier for potential property owners due to the large amount of cash required to either buy an existing leased property or convert a property for this purpose. In addition, limited lending options make it difficult to refinance and invest less money in the property.

Social housing properties are only available in areas where there is demand from housing associations or local authorities, which may not be local to the owner. Finally, because vulnerable tenants occupy social housing, housing associations have strict criteria for properties they will rent, which may make it more expensive to install the necessary features if the property was not previously used for social housing.

How much do I need for Social Housing?

Cash Requirement

As we've discussed, Social Housing can be one of the more cash-intensive strategies for Buy-To-Let property but the range will vary depending on the type of property used and whether you intend to buy one with an existing lease or intend to convert the property yourself.

On the lower end of the market, apartments are available in specific social housing blocks that can be purchased at lower prices. These properties can either be purchased as existing social housing or can be bought off-plan while still under construction. To purchase one of these apartments, you would likely need a starting budget of approximately £130,000 in cash, depending on location.

Depending on the house prices in the local area where the properties are needed, a starting budget of around £150,000 could be sufficient to purchase and convert a property for use as social housing. However, there are various factors that can influence this approach, and the actual cost may be significantly higher, particularly if the property requires extensive repairs or renovations.

Another way to own these properties is by purchasing a larger freehold property, which is usually converted to an HMO, has a lease in place with a housing association, and is already tenanted. The cost can vary depending on the location and condition of the property, but for a good starting point, a budget of around £100,000 should mean there are some opportunities available to you.

Sourcing, Converted and Securing the Lease

We've scored this one a 5 out of 5 difficulty if you're trying to source, convert and negotiate your own Social Housing.

Sourcing a property for Housing Associations can be difficult, especially if you're not local to the area in demand. You may face challenges in negotiating a property within your budget, organising and managing necessary contractors, all while ensuring that you meet the requirements set by the Housing Association to meet their standards. Even experienced property owners can find this process challenging.

Additionally, negotiating the lease particulars with the Housing Association to get the best returns can be a daunting task. However, if you manage to get through this hurdle, the ongoing management of the property should be relatively easy with the Housing Association managing the majority of it.

We've scored the other route to owning Social Housing as a 2 out of 5 difficulty.

Purchasing a property that is already being used for social housing or is being constructed exclusively for this purpose is a simpler way to begin with this buy-to-let strategy. Although this method is generally more expensive than doing it on your own, it eliminates a lot of the challenges involved.

The main issue with this option is the limited supply of these properties on the open market, which can make finding them time-consuming.

When the property is under contract with the housing association, the owner's management responsibilities are minimal, much like the DIY route.

Purchasing Existing

Level of Difficulty

How much work is involved with Social Housing?

Owner Involvement

When the purchasing element is removed from the equation and you focus on the ongoing ownership, Social Housing is one of the most hands-off strategies available in the Buy-To-Let market.

The Housing association lease the property from the owner and acts as the tenant, eliminating the need for the owner to interact with the occupants themselves. Additionally, the Housing Association is responsible for paying the rent to the owner, regardless of occupancy. They also handle any necessary repairs and maintenance of the property and must return it to the owner in its original condition.

Typical Returns & Timeframes

What should you expect from Social Housing Buy-To-Let properties?

Exit Strategy

What happens if you want to sell and how easy is it to liquidate your cash?

Social Housing properties which are leased to Housing Associations are usually held by investors for a long-term period to benefit from the lease. However, unexpected circumstances can arise, and in such cases, you may wonder whether it is possible to sell the property while the lease is still in effect.

The answer is yes, you can usually sell the property at any time, and the lease is typically transferred to the new owner on completion. The new owner will then start receiving rental payments.

However, selling this type of property may take longer than other strategies due to the cash required and limited financing options for the new buyer. Therefore, it is essential to find the right audience when marketing the property as simply listing it with a high-street estate agent may not result in a quick sale.

Frequently asked questions

What is a social housing HMO and how does it work?

A social housing HMO (House in Multiple Occupation) is a property rented out to three or more unrelated individuals, with each having a private room but sharing communal facilities. In a social housing investment model, the property is leased to a housing provider, who takes responsibility for finding tenants, managing the property, and maintaining compliance with housing regulations, plus they pay you the rent directly.

Why should I consider social housing HMO investment?

Investing in a social housing HMO offers hands-off income, long-term lease agreements, and contracted rent paid by the housing provider. It’s a reliable tenancy option for landlords seeking steady returns and reduced tenant management.

How does investing in social housing compare to standard buy-to-let?

Social housing investing offers more security than a traditional buy-to-let. Instead of managing tenants yourself, a housing provider handles the day to day running of the property without the need to pay a letting or property agent. This means no void periods, no tenant issues, minimal maintenance issues and often higher net returns for investors looking for a less stressful rental model.

What returns can I expect from a social housing HMO investment?

Returns on social housing HMOs typically range from 7% to 11% net yield, depending on location and lease terms. Because rent is contracted by a registered provider, many social housing investors see it as a lower-risk way to generate consistent income.

Are social housing HMO investments suitable for first-time landlords?

Yes, once let to a housing provider, social housing HMOs are ideal for first-time landlords. The housing provider manages tenants and maintenance, making this a passive way to start social housing investing without needing prior landlord experience. However, trying to secure a social housing lease on a new or existing HMO can be a very difficult and time-consuming process for even the most experienced property investor.

What are the risks involved in investing in social housing properties?

Like all investments, social housing HMOs carry some risks. These include potential changes to government housing policy or funding. However, long-term contracts and contracted rental income make social housing investing one of the more secure buy-to-let strategies.

How do I finance a social housing HMO investment property?

Most investors fund social housing HMO purchases with cash or bridging finance. Many sellers do not accept purchases with a buy to let mortgage. If they do, you will require specialist buy-to-let mortgages. Some lenders offer mortgage products specifically for social housing investment, depending on the term of the contract and the tenant type, so it’s well worth speaking to an experienced mortgage broker who is familiar with this type of contracted lease.

What types of properties qualify for social housing HMO use?

Social housing HMOs are usually freehold properties with 4+ bedrooms, fully renovated to meet HMO and safety standards. They must have proper licensing and meet local authority criteria to be leased to a housing provider. The housing providers typically have an extensive specification list of their own that HMOs must meet in addition to the local authority criteria before they are willing to lease the property.

How are tenants placed in social housing HMOs?

The housing provider is your tenant, and they are responsible for placing occupants, often termed "service users" in the property, not the landlord. Service users are usually individuals or families on housing support. The provider ensures placements meet the agreed tenancy type, helping reduce risk and void periods for the property investor.

How do I get started with social housing HMO investing?

To start investing in social housing, partner with a reputable property professional who has social housing HMOs for sale. There are options to purchase properties with the lease already in place, reducing the risk for the new owner, or options where you can attempt to secure your own from a social housing provider. Make sure the lease terms are clear and you understand both the tenants' and your obligations as the landlord, the housing provider is established and well funded, and the return aligns with your goals.

Registered Company Number: 15439671

Copyright © 2025 Seven Generations UK Limited, All Rights Reserved

PRS Membership Number: PRS043981

Your trusted partner for UK buy-to-let property

Quick Links

Contact Us

ICO Membership Number: ZB694046

Properties For Sale